Opportunity Zone Investing Series: Heads I Win, Tails We (the US Treasury & me) Lose

Over the next few weeks I will be describing several dimensions of the evolving Qualified Opportunity Zone (QOZ) program, which was legislated into existence by way of The Tax Cuts and Jobs Act of 2017 and seeks to compel investors, by way of attractive tax incentives, to harvest unrealized capital gains and invest this capital into qualifying entity-level and real estate investments in select low income (and low income adjacent) census tracts. My intent is to provide a balanced view of the program along a range of topics, including investment strategy, asset and investment manager selection and access, program incentives and unintended consequences, program intent and expected efficacy, and material tax code issues outstanding. The program represents a unique chance for investors to earn excess after-tax expected returns, but its notable that there are several tax code interpretation and program execution issues outstanding regarding which the IRS must provide guidance (e.g. clarifying language and inconsistencies, clearing unintended execution complexities) that create compliance risk for the end investor. Today we begin with a discussion of the structure of the tax benefits and its implications for investors.

Tax Benefit Structure

We begin with an example of a $100 capital gain that our hypothetical investor (“Investor”) plans to harvest and invest in a QOZ. The gain could come from any asset class, and unlike the 1031 Exchange program, wherein Investor must invest the entirety of its sale proceeds to avoid a taxable event, in this case, Investor only need reinvest the capital gain to defer taxes. We will discuss elements of the technical process the IRS has designed in a future posting (simplifying below for clarity). While capital gains harvested in 2017 are eligible for investment (requires filing an amended tax return), going forward, an investor will have 180 days after selling a position to reinvest the capital gains into a Qualified Opportunity Zone Fund (QOZF), which then invests the capital in assets or business entities. Note that the QOZF is just a corporation or partnership formed to invest in QOZs (name does not imply a commingled closed ended private equity fund).

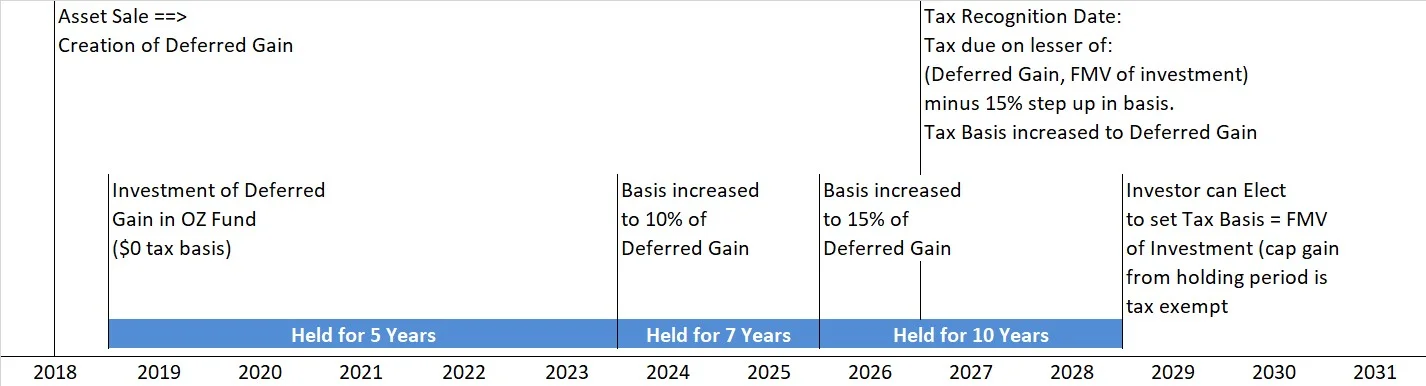

Tax Event Timeline

Investor rolls a $100 capital gain, from any asset class, into a QOZF that then deploys it, (pure gain so zero tax basis on day one):

- The $100 gain is deferred until the earlier of exit or Dec 31, 2026.

- After five years, Investor receives a 10% step up in basis to $10.

- After seven years, Investor receives an additional 5% step up in basis to $15 == > tax on this $100 deferred gain goes from $23.8 to $20.2 (using today’s Federal capital gains rates; New York is the only state to have announced that it will provide the same benefits regarding state capital gains tax).

- Dec 31, 2026 Tax Recognition Date: Unless Investor has previously exited, Investor pays tax on the lesser of Deferred Gain ($100) and investment’s fair market value (FMV), minus the 15% step up in basis. At this point the Investment’s tax basis is set to the initial deferred gain of $100 (may require Investor to reserve funds or recapitalize to generate liquidity for tax payment).

- After 10 years, at exit, Investor may elect to set tax basis of Investment = FMV. E.G., if the $100 initial Investment is now worth $300, Investor may elect to set the tax basis of Investment ($100 after step 4) to $300, exempting holding period capital gain from taxes.

Notably, one could interpret points 1 – 4 above as the US Treasury extending Investor a zero-interest “equity loan” wherein:

- US Treasury contributes (at today’s federal capital gains tax rate) 23.8% of the equity yet captures none of the returns;

- If Investor holds > 7 years, and Investment has increased in value, Investor repays the Treasury only 85% of the initial principal (holding applicable capital gains tax rate constant), and;

- If Investor holds > 7 years, and Investment has decreased in value, Investor repays the Treasury only (Investment FMV / Initial Investment) minus 15% of the initial principal. E.G., if FMV = $50, Investor would owe tax on $50 - $15 = $35. The Treasury participates pro rata in any reduction in investment fair market value (FMV) as of Dec 31, 2026.

Examining the structure, one could note that the main effect is to amplify returns. Tax deferral (the zero coupon “equity loan”) and the exemption of holding period capital gains in year 10 collectively serve to increase volatility to the upside, with the bulk of the benefit flowing from tax deferral. The benefits of both are directly proportional to the returns an investment generates from appreciation. When a deal generates a 10% net IRR over 10 years with half of the returns coming from current cash flow versus appreciation, this incentive program can boost the corresponding after-tax net IRR by approx. 300bps (setting aside differences in depreciation and depreciation recapture across scenarios and other complexities). The increases in tax basis in years five and seven are quite minor when spread over 10 years.

What this means for Investors

Investment strategy and execution are still primary. The tax benefits serve as an amplifier of returns, albeit with the US Treasury sharing in the downside. Despite the return asymmetry this sharing in the downside engenders, if Investor’s initial investment of $100 turns into $90 as of the end of 2026, Investor still loses $7.60. As such, if an investment manager pitching this program does not have a convincing investment thesis and track record of sourcing and execution, if you wouldn’t feel comfortable writing a check to said manager without the Opportunity Zone overlay, the overlay should not compel you to do so. Friends in the family office space note that they are getting substantial inbound inquiries from would be investment managers. In my view, the program’s benefits depend too extensively on investment performance to take substantial manager risk without levers to control it.

In a subsequent posting we will spend more time on manager and investment selection. Suffice it to say that in either case, regardless of the powerful but “perishable” deferral benefit, prudence trumps speed.