Unison Homes: Enlightened or Extractive Capitalism?

As noted in our Divvy Homes analysis, the market has seen a proliferation of sometimes innovative, sometimes value-creating venture-backed home ownership models. This series aims to provide a look beneath the corporate veneer to discern which firms create value for users, investors, and society. Why society? Most of these firms claim to advance a social mission, which is particularly true with the firm I discuss today.

Unison is a home ownership model created by a group of Wall Street veterans that fits roughly within the down payment assistance segment. According to its website, Unison “…is pioneering a smarter, better way to own homes…We believe in a world where owning a home is not a zero-sum game, and that with the right partners, everyone can win.” It later states that “We are radical enablers of enlightened capitalism pioneering optimal homeownership for all.” These are pretty strong claims of social impact. According to our analysis below, Unison’s model appears to create value mainly if not only for investors and in a manner that is largely zero sum with users, presenting a form of capitalism that looks more extractive than enlightened. Ethical overlay notwithstanding, risk-adjusted gross returns to Unison’s investors should be highly attractive.

How it Works

Unison offers its equity HomeBuyer co-investment program as well as a home equity cash-out refi offering; we will focus on the former. Unison can match a user’s equity investment in a home, investing between 5-20% of a home’s value in equity ($500k max for up to 30 years). This unique joint venture arrangement requires that users utilize Unison-approved lenders (likely at higher cost given fewer competitors). Unison claims it charges users a 2.5% fee for it to invest on one page and 3.9% on others; we will assume 3.9%. Because those seeking to partner with Unison are cash constrained, our hypothetical user in scenarios below purchases with 20% down (Unison provides half).

Unison does not take a conventional equity stake in the property, such that it is subject to the typical SFR’s 80% leverage on its position. While it is contributing half the equity by contributing 10% of the home’s value (subject to differences mentioned below), Unison does not collect its pari passu 50% share of appreciation. Instead Unison invests in the unlevered asset. Per the deal level return table below, it is thereby able to circumvent meaningful transaction costs.

Unison’s agreements are structured as option contracts, which are structured in favor of the Wall Street veterans. The mechanics from Unison’s website are provided here in Unison’s infographic along with a more detailed Rampart Ridge analysis that describes what the user gets net of fees (example home is based in San Francisco; fees will vary by state and municipality). Unison provides the user with 10% of the home’s purchase price up front, which purchases 10% of the home’s value. Unison does not cover its pro rata share of transaction fees, so this is equivalent to purchasing 10% for the cost of 9%. In the agreement, the user also writes Unison an at-the-money call option to purchase 30% of the home’s value at exit in exchange for an at-the-money put option obligating Unison to buy 30% of the home’s value at exit. This enables Unison’s four times the exposure to asset appreciation/depreciation as the size of its initial unlevered investment in the home.

Value for Users

As we have seen with Robinhood, unskilled options daytraders get slaughtered by failing to understand the complexities of gamma hedges, volatility, etc, and by trading with quants who do. Similarly Unison’s users have no ability to value the options they are trading, evinced by the wide spread in value the user gives up relative to what it receives.

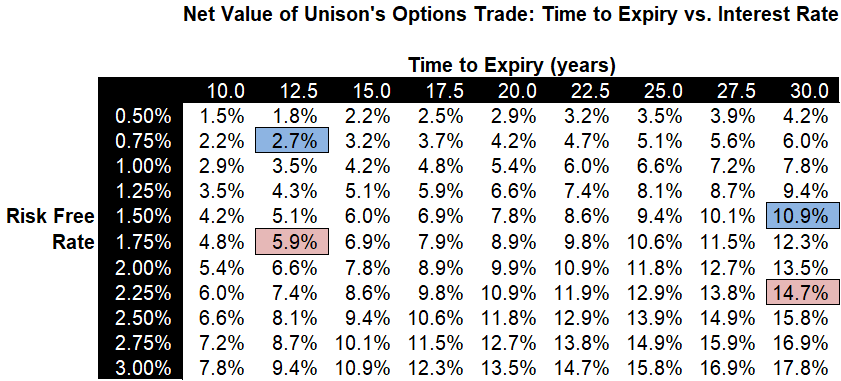

This table depicts the value of the call option Unison receives from the user minus the put Unison gives the user (as a % of home value). The blue cells describe our estimate of the net value Unison gains if its users hold 12.5 or 30 years on average at today’s ultra-low rates. The red cells reflect the same but at risk free rates that applied one year ago. Unison’s call options are intuitively incrementally less valuable than standard European options in that time to expiry is chosen by the user.

To estimate the value of this spread (leaning on my b-school derivatives class so don’t want to overstate my level of accuracy), I used Black Scholes and binomial pricing models and assumed 15% home value volatility and no early exercise across a range of risk-free rates and times-to-expiry (see inset). If we parameterize for 30 years to expiry, the value of Unison’s call option is ~47% of its strike price or 14% of the home’s value, with the put worth 4% of the home’s value (==> by trading a call for a put, Unison gains 14% - 4% = 10% of the home’s value at no cost). Of course, time-to-expiry is not fixed in Unison’s deals, it is determined by the user, which intuitively should decrease the value of Unison’s call option relative to the user’s put (although not by much if the value delta between equivalently parameterized American & European options is any indicator).

To estimate time to expiry, we look at Redfin & NAHB data, while realizing that Unison has a team of quants on board that can maximize returns by investing in MSAs and specific home & user profiles to solve for the profit maximizing combination of expected appreciation, hold period, and MSA level SFR volatility. According to Redfin, in 2019, the typical household had spent 13 years in its home, with average hold period ranging from 5.2 yrs in Grand Rapids, MI to 23.4 yrs in Salt Lake City, UT. In 2013, the NAHB calculated that first time homebuyers were staying, on average, 11.5 years, although Redfin believes holding periods are expanding. In the case where time to expiry = 12.5 years, Unison captures 2.5% of the home’s value in this options trade (if we round down to reflect user’s control over expiry). This is an interest rate sensitive calculation; this figure was 5.5%-6.0% of home value 12 months ago.

For a hypothetical home based in San Francisco (priced to dovetail with Unison’s website exhibit), the above provides a more realistic picture of returns to each party. Whereas Unison earns a 1.8x multiple on its equity, the user only breaks even, absorbing all transaction fees.

Unison’s Multiple: If Unison exercises, its strike price of 30% of initial home purchase price is paid through escrow at sale, concurrent with user’s payment to Unison of 40% of the sale price (we net the payments and divide by the only capital Unison actually sends the user before exit). Unison’s option structure enables it to invest 10% while earning returns on 40%, amplifying its IRR. It also gets paid based on the increase in gross exit price over purchase price (user alone being responsible for $60k in fees). The user can lose money on the deal and still owe Unison a return on its capital (not what I would call “true partnership”).

User’s Multiple: Due to user’s responsibility for all fees, Unison always outperforms the user in terms of returns.

This exhibit depicts the various multiples each party earns on its equity depending on appreciation rate. Note that despite Unison’s claim to presenting “true partnership,” its equity multiple greatly exceeds that of the user.

Breakeven Scenario: Unison gets paid a percentage of the extent to which the sale price exceeds the purchase price. If user sells home for the purchase price (appreciation rate = 0%), user pays the $54k in fees in column two and ends up losing $54k before having to return Unison's $50,000 investment.

1.50-1.85% per annum appreciation still results in a user loss. Between appreciation rates of 0.0% and 1.0%, Unison gets paid returns on capital despite a deal-level loss (user getting diluted). This is because it is paid based on the increase in sales price over purchase price instead of net proceeds over investment cost.

Unison captures > 49% of upside across these scenarios, more than the 40% presented in its incomplete math. Furthermore, Unison earns a multiple on its equity invested that exceeds that of the user by between 0.1x and 1.2x depending on deal performance.

Additional transaction asymmetry resides in the payment of transaction fees and asset preservation capital. In addition to paying all acquisition and disposition related fees, the user pays all property taxes, insurance, HOA fees, repairs and maintenance, and capex for asset preservation. In contrast, when renting, the landlord pays all such expenses (plus utilities in some circumstances). The nuance here is that the user shares the landlord position with Unison and serves as sole renter. Since the user gets use of the home and thereby avoids paying rent, it makes sense that it is paying for the OPEX its rent is meant to cover. While even NNN leases place the burden of maintaining a structure’s core & shell on the landlord (jointly the user & Unison, pro rata), NNN leases involve the payment of rent. If I had to assert what I thought was fair, it would be that Unison should share in acquisition and disposition related fees pro rata, with capital paying OPEX/CAPEX (pari passu between Unison & user), and the user paying market rent.

Value for Investors

Unison offers investors in its PropCo the chance to earn above market gross returns on investments in the large residential housing sector. While we don’t have insight into fund terms, in terms of gross returns, the product offers a host of advantages to investors, which derive from two main sources: 1) the offloading of pro rata transaction fees and asset preservation CAPEX onto users, and 2) the options trade users likely don’t understand. Combining 1) and 2), and at today’s ultra low risk-free rate, Unison is purchasing $1.25 in value for $0.90 every time it closes a deal.

If we could set ethics aside, financial investors should be thrilled with a model that can provide exposure at scale to a lower correlation asset class with such pronounced deal structure advantages. For example, I would strongly consider a investing in a model that could execute an analogous strategy for owner-occupiers of commercial buildings. Mid- to large-cap businesses have no excuse for getting out-negotiated by an investor; they are not orphans or widows and can afford skilled advisors.

However, ethics matter. When a team of Wall Street derivatives experts target, as counterparties, those aspiring homeowners with insufficient wealth afford a down payment (no knowledge of derivatives) and convinces them to trade $1.25 (or $1.55 at last September’s risk free rate) in value for $0.90, that is not what I would call “enlightened capitalism” or the biproduct of the “virtuous machine” Unison claims to be building.

I question how a pension fund CIO could justify investing in a product that would extract wealth from people who could be amongst its plan participants (similar tax bracket). Were PF participants to use Unison, it would then be extracting wealth from users to: 1) pay Unison’s VC backers and founders in fees, and 2) give the pension fund a fraction of what its plan participants lost. Why not just ask the plan participants for their money directly, circumvent the middlemen and invest the proceeds in INVH? If institutional investors seek exposure to the residential asset class, they should structure fair and transparent deals with homeowners and reserve complex structuring for the way they lever their position. If Unison wants to reduce the volatility of it’s position, it should buy calls and puts in the market instead of forcing home buyers to unknowingly become options traders while assuring them that their title companies will handle the math.

Unison raised a series B in 2018 and has been raising funds for its PropCo from endowments and pension funds who apparently lack interest in the ethical overlay. If the capital cares purely about performance, Unison should thrive. Its model offers attractive risk-adjusted returns with the same underlying risk factors as residential housing but with superior expected returns. While the complexity of the structure could provide some drag on Unison’s ability to scale users, per the infographic above, Unison likely leans heavily on the simplified description of its model that omits mention of options altogether.

Value for Society

“Any claims of improving homeowner financial health or retirement savings should be offset by this substantial extraction of homeowner wealth.”

“Unison Investment Management delivers social impact by enhancing home affordability, improving homeowner financial health, and closing the retirement savings gap.” While it does enable users to reduce monthly fixed costs (hence default risk), possibly avoid mortgage insurance (mortgage interest rate may be incrementally higher) and possibly allow users to improve asset allocation by diversifying into other asset classes, it does so at a very high cost to users. In the example above, if we assume that Unison should pay fees equivalent to its percentage of the appreciation, the user cedes $36k (down from $51k at last year’s risk free rate) in pro rata transaction fees and option value to Unison in exchange for only $48k in co-investment equity. Any claims of improving homeowner financial health or retirement savings should be offset by this substantial extraction of homeowner wealth.

To estimate Unison’s benefit to users, we could estimate the disparity in default probabilities across scenarios wherein the user is 90% levered vs. receiving 10% from Unison and then calculate the resulting value destruction from a forced sale. We could also simulate the portfolio benefit to the user investing half of its 20% down payment in equities and fixed income instead of investing solely in SFR equity that is at risk precisely when the user needs savings most (loss of job). However, the quick math is that if a user partners with Unison to fund its $100k down payment per the example above, Unison provides the user with $48k net, but reduces the user’s net worth by $36k in the process, leaving it $12k (< $0 at last September’s risk free rate) to diversify into other asset classes. Its unlikely the user could earn sufficiently high returns on this $12k in diversified exposure as it could by leaving the $48k invested in its home (holding portfolio risk constant across scenarios). Is the comparison favorable if including the impact of reduced default risk? Neither of Unison’s benefits justify it charging such an egregious price for co-investment equity; I suspect users would decline the trade if they understood it.

Conclusion

Unison was designed with investors in mind; it offers a thoughtfully-designed financial product that should provide highly-attractive risk-adjusted returns to investors. As such it may satisfy its website claim of being a smarter, better way to own homes, but more likely for Unison’s investors than for its users. Returns to investors within an asset’s capital structure are zero-sum, such that excess returns to investors come at the expense of users ill-equipped to evaluate Unison’s complex offering. Furthermore its social impact story is heavily diluted if not negated by its extractive structure (excess returns in exchange for impact dilution).

***

Certain information contained in here has been obtained from third-party sources. While taken from sources believed to be reliable, Rampart Ridge, LLC has not independently verified such information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation.

This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by Rampart Ridge, LLC. (An offering to invest in a Rampart Ridge, LLC fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety.)

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.